Best Places to Work and Live in the GCC in 2026

Overview of the Gulf’s most dynamic cities

The Gulf Cooperation Council has never been more competitive for international talent. Eight cities, each with its own personality, pace, and promise, are collectively reshaping what it means to build a career in the Middle East. Whether you’re drawn by tax-free salaries, mega-project pipelines, or a quieter quality of life, this guide cuts through the noise and gives you a city-by-city picture of where opportunity and livability actually converge in 2026.

The Cities at a glance

Dubai remains the region’s undisputed commercial capital, the city most people picture when they think of GCC opportunity. Its Financial District, free zones, and DIFC make it the default landing pad for finance, tech, and media professionals. The trade-off is a higher cost of living and fierce competition for roles.

Abu Dhabi is the quieter, wealthier sibling. The UAE capital is home to ADNOC, Mubadala, and a growing cluster of sovereign-backed institutions. It ranks safer than Dubai on most indices and typically offers more generous public-sector packages, with a noticeably more relaxed pace.

Riyadh is the region’s fastest-moving story. Saudi Arabia’s capital is in the midst of a historic transformation, pouring investment into entertainment, tourism, and technology under Vision 2030. Expatriate life has opened up dramatically in recent years, and the sheer volume of infrastructure spending makes it an attractive market for engineers, project managers, and consultants.

Doha punches above its weight for a city of its size. Qatar Energy’s influence keeps energy-sector salaries high, and the country’s post-World Cup infrastructure (from Lusail City to a modern metro) has raised the bar for everyday life. It’s compact, safe, and cosmopolitan.

Muscat is the GCC’s best-kept secret. Oman’s capital offers a genuinely affordable lifestyle, dramatic coastal and mountain scenery, and a pace that feels more human than its UAE and Saudi neighbors. It’s not the city for those chasing the highest absolute salary, but for value-adjusted quality of life, it is hard to beat.

Jeddah is Saudi Arabia’s commercial and cultural heartbeat on the Red Sea. It’s more relaxed in temperament than Riyadh, with a strong retail and hospitality sector and a growing role in tourism as the country develops its coastline.

Manama is Bahrain’s compact capital and a long-standing financial hub. Its proximity to Saudi Arabia (connected by the King Fahd Causeway) makes it attractive to professionals who want a liberal social environment within commuting distance of the Kingdom’s job market.

Kuwait City remains primarily an oil economy, with strong government salaries and a stable, if quieter, professional scene. Opportunities outside the public sector are narrower than in the UAE or Saudi Arabia, but the cost of living is reasonable and the community tight-knit.

The conflict that changed the conversation and the one that didn’t change daily life

Nobody who lives in the Gulf will forget the morning of February 28. At around 1:15 a.m., US and Israeli forces launched Operation Epic Fury, a coordinated campaign of nearly 900 strikes targeting Iranian military leadership, missile infrastructure, air defense systems, and IRGC command nodes. The opening salvo killed Supreme Leader Ali Chamenei. Within hours, Iran had begun retaliating across the entire region, and the GCC found itself absorbing the consequences of a war it had no hand in starting.

The speed of it was disorienting. Before most residents had left for work that Saturday morning, alerts were going off across Gulf cities. Iran’s retaliatory strikes targeted US military installations in Kuwait, Qatar, Bahrain, and the UAE, but they did not stop there. Hotels, airports, ports, desalination plants, and energy infrastructure all came into the crosshairs in the days and weeks that followed. Iran’s stated aim was to damage the GCC’s reputation for economic stability and pressure Gulf governments into pushing Washington toward a ceasefire. The strategy was deliberate and, in the short term, effective at generating fear.

Across the region, approximately 40,000 flights were cancelled as airspace closures severed the Gulf’s connections to the global economy. The economic toll was real. Oxford Economics downgraded GCC GDP growth forecasts by 1.8 percentage points to 2.6% for 2026. The tourism sector, particularly in the UAE, took a sharp hit. The Strait of Hormuz closure disrupted oil exports and pushed energy prices globally. Supply chains backed up. Some expatriates left.

And yet the overwhelming majority stayed. That is the more telling part of the story.

Local security forces and air defense systems, supported by the US military, intercepted the bulk of Iranian projectiles. By week five of the conflict, interception rates had risen from 46% to over 70%, and the volume of attacks had declined significantly. Casualty figures in the GCC, though tragic for those affected, were remarkably low given the volume of strikes: 13 people killed in the UAE, 10 in Kuwait, 3 each in Bahrain, Saudi Arabia, and Oman across the entire duration of the conflict. Gulf governments moved quickly to reassure residents. The rulers of Dubai walked through the Dubai Mall days after the initial strikes to signal that the city was open and safe. Emergency protocols activated smoothly. Supermarkets stayed stocked. The banking system kept running. Offices reopened within days.

A ceasefire between the US and Iran was announced on April 8. Major airlines including Emirates, Etihad, Qatar Airways, and Saudia began rebuilding flight schedules cautiously but steadily. The Strait of Hormuz reopened to commercial traffic. By mid-May, the rhythm of the Gulf cities had largely returned: the malls were busy, the restaurants were full, the construction cranes had not stopped turning.

What does this episode mean for someone weighing a move to the GCC?

A few things are worth saying plainly.

The conflict exposed something that had always been true but rarely tested: Gulf cities are geographically close to Iran, and the region’s defensive architecture, however effective, cannot make the risk zero. Analysts at the Qatar-funded Middle East Council on Global Affairs described the war as having “shaken” the Gulf’s image as a region immune to conflict. That is a fair assessment of perception. The physical disruption, however, was significantly contained.

Millions of expatriates chose to stay during the conflict, a more meaningful vote of confidence in the region than any survey. The social contract that Gulf governments maintain with their populations (security in exchange for loyalty to the ruling compact) was tested and, for most residents, held. Time magazine noted that in places like Dubai, “millions of expatriates have put down roots and appear more inclined to wait out the conflict.”

With the ceasefire holding and flights resuming, economists expect trade and domestic activity to recover gradually through the second half of 2026, with stronger catch-up growth forecast for 2027. The fundamental economic case for the GCC (the megaprojects, the diversification investment, the tax-free salaries, the global connectivity) remains structurally intact.

The conflict is a chapter, not a conclusion. The GCC’s cities were not broken by the events of February through April 2026. They were shaken, stressed, and in some cases visibly scarred, but they kept going. For most people living and working here, the most accurate description of the experience is not drama but dogged continuity: alarm notifications on phones, news updates at lunch, and then back to the meeting.

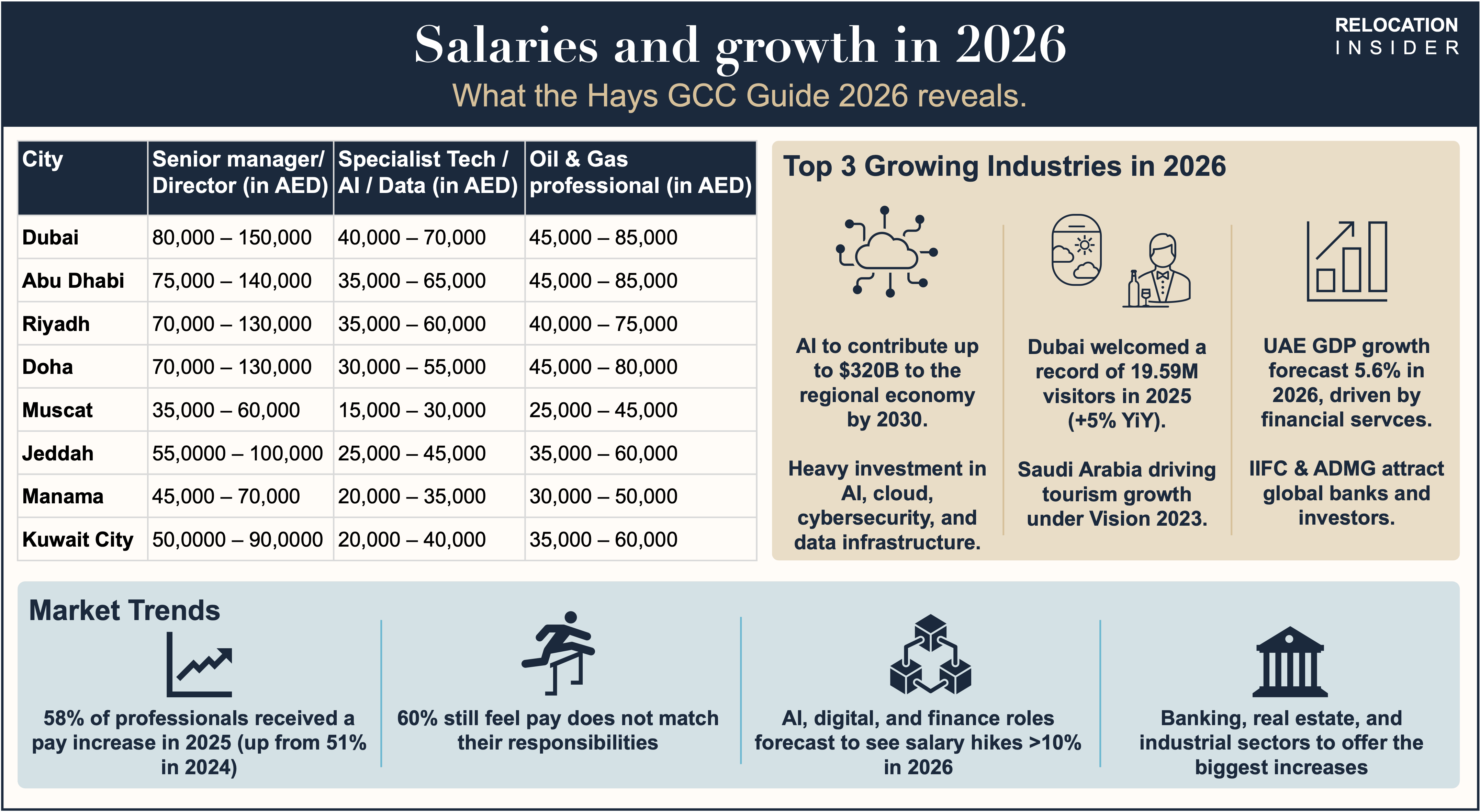

Wage rankings: The Hays GCC Salary Guide 2026

The Hays GCC Salary Guide 2026, now in its 12th edition, covers salary data for nearly 400 roles across 11 sectors and draws on a survey of over 1,600 employers and professionals across the Gulf. It is the most comprehensive public benchmark available for the region.

The headline finding is a market under productive tension. Salary optimism is rising: 58% of professionals received a pay increase in 2025, up from 51% in 2024, yet 60% still feel their pay does not match their responsibilities. That gap tells you something important: the Gulf is hiring aggressively, but compensation frameworks haven’t fully caught up with expectations shaped by inflation and global competition.

Dubai leads in absolute corporate and technical compensation, with senior professionals in finance, technology, and legal roles commanding the highest packages. Its attraction isn’t just the number; it’s the zero-income-tax environment that makes the net figure compelling. CEOs in Dubai earn AED 80,000 to 150,000 per month, CFOs AED 70,000 to 120,000, and AI/data specialists AED 40,000 to 70,000.

Riyadh has emerged as a fierce competitor for executive talent, aggressive on cash salaries, with strong bonuses particularly in corporate banking, investment banking, and energy infrastructure roles driven by Vision 2030 project pipelines. Saudization targets do, however, constrain the tenure outlook for expatriate roles in some sectors.

Doha offers a smaller but often more focused market. Oil and gas professionals, the backbone of Qatar’s economy, earn QAR 45,000 to 80,000 per month, with key employers including QatarEnergy. The energy sector continues to anchor compensation at the top end.

Abu Dhabi sits broadly in line with Dubai for senior roles, with a notable premium for government-linked positions. Packages in the public sector frequently include housing allowances, school fees, and end-of-service benefits that substantially lift total compensation above the base salary.

Muscat, Manama, and Kuwait City offer lower absolute wages than the UAE or Saudi hubs, but significantly lower costs of living, particularly in rent, which softens the difference in purchasing power.

Specialized roles in AI, digital transformation, and finance are expected to see salary hikes exceeding 10% in 2026, with the banking, real estate, and industrial sectors forecast to offer the most substantial increases across the region.

Top 3 Growing Industries in 2026

1. Technology and Artificial Intelligence

This is the defining investment theme of the decade across the GCC. According to PwC Middle East, AI is expected to contribute up to $320 billion to the regional economy by 2030, with the GCC leading adoption. Governments are investing in sovereign AI infrastructure, advanced data centres, cybersecurity frameworks, and cloud ecosystems. Saudi Arabia and the UAE are driving this, but Qatar and Bahrain are building AI and fintech capabilities at pace.

2. Tourism and Hospitality

The Gulf’s pivot from oil to visitor dollars was accelerating fast before the conflict and remains a strategic priority coming out of it. Dubai ended 2025 with a record 19.59 million international overnight visitors, a 5% increase on 2024 and the third consecutive year of record-setting growth, with more than two million visitors in December alone. Saudi Arabia is the newer story: tourism, finance, and sustainable energy are central to the Kingdom’s diversification push, with non-Saudis now permitted to purchase real estate in specific areas from January 2026, a move expected to attract significant foreign investment once confidence returns to pre-conflict levels.

3. Financial Services and Fintech

The UAE is forecast to post GDP growth of 5.6% in 2026, driven partly by financial services alongside tourism, trade, and population growth, under the “We the UAE 2031” strategy. Dubai’s DIFC and Abu Dhabi Global Market continue to attract global banks and investment firms. In Bahrain, fintech has become a national priority, and Riyadh is building its capital markets infrastructure at pace to support Vision 2030 privatizations and listings.

Quality of life rankings

The data here is clearer than the salary picture, and the GCC performs remarkably well by global standards, particularly on safety.

Numbeo’s 2026 Safety Index (covering 400 cities globally) puts the GCC’s cities among the world’s best. Abu Dhabi retained its position as the world’s safest city for the tenth consecutive year. Doha ranked fourth worldwide, Muscat eighth, Riyadh 34th, Jeddah 40th, and Kuwait City 73rd.

Mercer’s Quality of Living Survey places the UAE’s two main cities near the top of the Middle East. Dubai ranks 83rd and Abu Dhabi 85th globally, both recognised for modern infrastructure and diverse expatriate communities, though Dubai faces challenges around traffic and climate-related concerns.

Numbeo’s full Quality of Life Index for 2026 gives Muscat a score of 189.22, placing it 58th globally. Oman scores very high on purchasing power (116.41) and safety (81.33), while maintaining a very low cost of living index (45.11) and extremely manageable commute times.

IMD’s Smart City Index 2025 includes both Dubai and Abu Dhabi in its global top five, the only non-European cities to feature, recognising their digital infrastructure and governance quality.

The consistent picture: UAE cities lead on safety and infrastructure; Muscat leads on affordability and liveability balance; Riyadh is rapidly improving but still catching up on social amenities.

From a personal lens: What life actually feels like

Rankings tell you where things land on an index. They don’t tell you that walking out of a Dubai Metro station in October and finding the air still warm at midnight feels electric in a way that no European city quite replicates. Or that Muscat on a Friday morning (corniche walk, no traffic, fresh fish at the market) is one of the Gulf’s genuinely underrated pleasures.

In Dubai, the pace is relentless and the opportunity is real, but so is the competition. The city rewards ambition and punishes stagnation. Rent is the single biggest lifestyle variable: the gap between a shared apartment in Deira and a one-bedroom in Dubai Marina can be the difference between financial comfort and monthly anxiety. During the conflict, it was also the city where you could feel the machinery of normalcy most deliberately at work, with government reassurances, open restaurants, and the Mall of the Emirates still humming on a Thursday night even as alert notifications lit up phones.

In Riyadh, the transformation is visible on every skyline and in every government initiative. Expatriates who arrived five years ago describe a city almost unrecognisable from what it was. Entertainment, dining, and social life have expanded dramatically. The city rewards patience: the projects are real, but bureaucracy can be slow, and building a social network takes longer than in Dubai.

In Doha, the community is tight. Expats who stay more than a year tend to stay much longer. The city is manageable in a way Dubai isn’t: distances are shorter, traffic is lighter, and the pace allows for a genuine life outside of work. The gas-sector connection means many professionals arrive on packages that include housing and schooling, making the net financial position very strong. Doha’s experience of the conflict was a sobering one (the strike on Ras Laffan was close to home for many energy workers), but the city’s response was orderly and community bonds held.

In Muscat, you trade opportunity for quality. Fewer roles, lower absolute salaries, but a life that doesn’t feel like it’s running at 1.5x speed. The natural landscape (mountains, wadis, coastline) is spectacular, and the Omani community is among the most welcoming in the region. Oman’s diplomatic channel with Tehran also meant Muscat was the least targeted GCC city during the conflict, a distinction that was not lost on residents.

In Manama, the Gulf’s most liberal social environment combines with easy access to Saudi Arabia’s market. For professionals commuting into the Eastern Province, Bahrain offers the personal freedoms of the UAE at a more manageable cost.

The bottom line for Relocation Insider readers

There is no single winner. The right city depends entirely on what you’re optimising for.

If maximum compensation is the goal, Dubai or Riyadh (with zero income tax on Gulf packages) remain the region’s strongest financial propositions, especially in technology, finance, and senior leadership roles.

If safety and quality of life are the priority, Abu Dhabi and Doha consistently top the rankings, offering world-class infrastructure in compact, manageable environments.

If affordability matters, whether for savings or simply for a life that doesn’t feel financially precarious, Muscat and Manama offer a level of purchasing power that Dubai simply cannot match at equivalent salary levels.

If career growth is the driver, Riyadh in 2026 may be the most interesting bet. Saudi Arabia’s non-oil economy was growing faster than any other in the region before the conflict and is expected to lead regional recovery. The professionals who build networks there now are likely to be well-positioned for the decade ahead.

One final word on the events of the past two and a half months. They have permanently entered the calculus of anyone considering a move to the GCC. That is appropriate, because risk transparency is part of an honest conversation. But the story that emerged from those months is not one of cities abandoned or economies collapsed. It is a story of institutions that held, air defenses that worked far better than many expected, and communities (expatriate and local) that chose to stay. The ceasefire of April 8 brought flights back, supply chains back, and restaurants back to full tables.

The GCC has always rewarded those who showed up and stayed. In 2026, staying turns out to be its own kind of statement.