The Ultimate Guide To Decide If You Should Rent First or Buy Immediately After Moving Abroad

A data-driven approach to making the smartest housing decision as an expat

Miguel is a friend of mine. I met him in Qatar over a year ago. He’s a 41-year-old finance manager from Madrid, and when his company offered him a corporate transfer to Doha, he said yes without hesitation. It was a career opportunity he couldn’t pass up: a proper package, a real step up, and Qatar was booming. He moved with his wife and two kids, full of energy and optimism.

Before the family even arrived, Miguel had been doing his research. He’d spent weeks on property portals, WhatsApp expat groups, and Google Maps. He knew the compounds, he knew the districts, or so he thought. And wanting to give his family stability from day one, he signed a two-year lease on a large villa in a well-known compound in the western part of the city. Spacious. Good security. Ticked every box on paper.

By month three, the cracks were showing.

The compound was beautiful but almost entirely populated by families from a completely different professional circle. His kids’ school was a forty-minute drive in Doha traffic, a commute that became its own kind of daily punishment. His wife, who had left a strong social network in Madrid, found herself isolated; the community on the compound simply wasn’t the right fit for her. And the area that turned out to suit them, closer to the school, closer to the friends they were slowly making, with the kind of neighbourhood energy they actually wanted, was on the other side of the city.

They were locked in. Two-year lease. No easy way out without a painful financial and legal conversation with the landlord.

Miguel’s story isn’t unusual. It’s the default for expat families who try to solve the “settling in” problem before they’ve actually settled in.

It has a name: signing before you know.

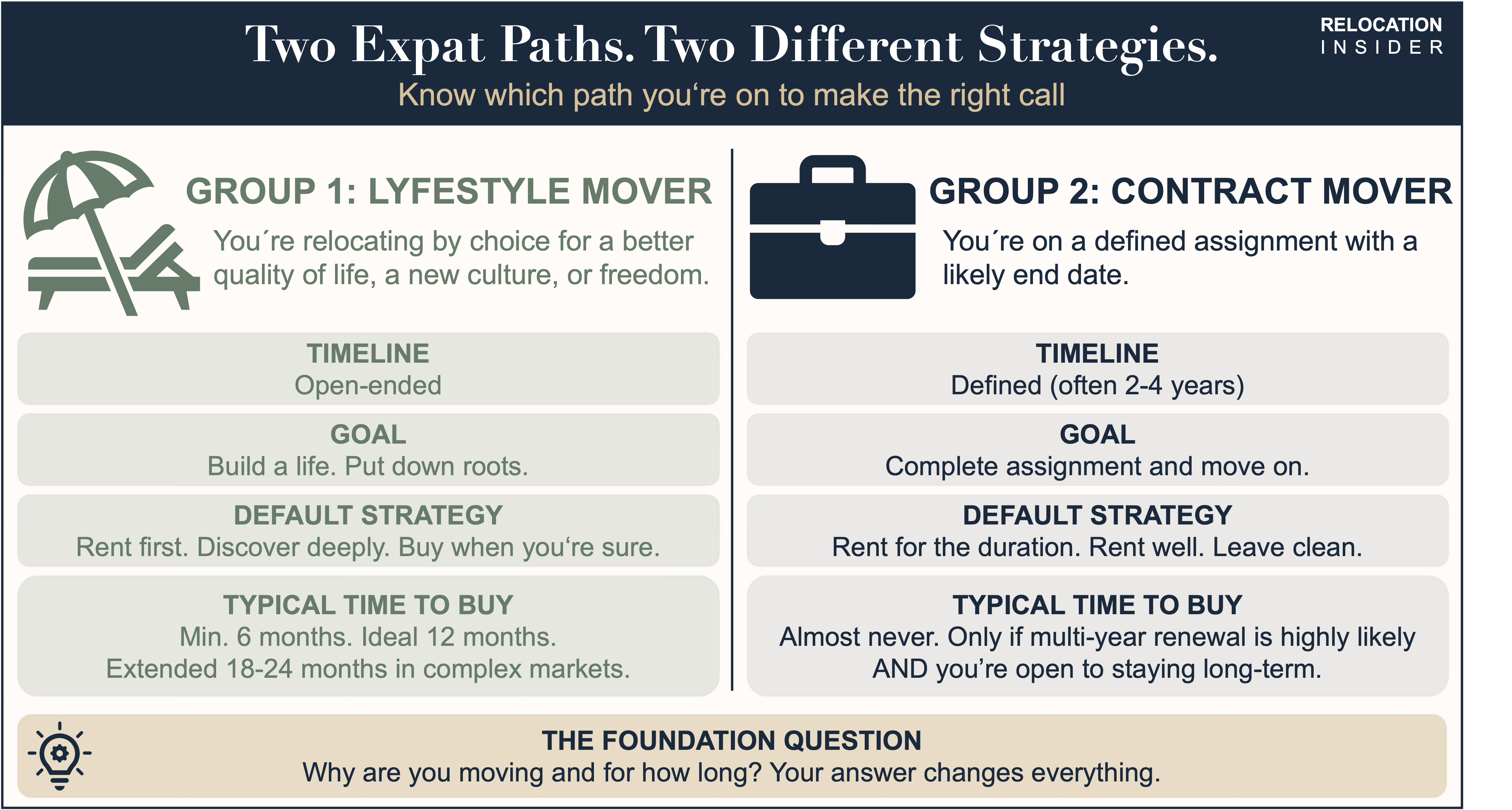

First, ask yourself the most important question

Before we even get to renting versus buying, there’s a foundational question that changes everything:

Why are you moving and for how long?

This matters more than almost anything else in this decision. Because the expat world broadly splits into two very different groups, and the right strategy for each is completely different.

Group one: the lifestyle movers

These are people relocating by choice, chasing a better quality of life, a lower cost of living, a new culture, or the freedom that remote work makes possible. Their timeline is open-ended. They’re not going back unless they want to.

Group two: the contract movers

This group is enormous, and chronically underrepresented in relocation advice. These are people moving for a defined assignment: a 2-year posting in Dubai, a 3-year contract in Singapore, a 4-year secondment in Jeddah. They have an end date, or at least a likely one. Their employer may be covering housing allowances. And their entire calculus around buying is fundamentally different.

If you’re in group two, read the next section carefully, because most conventional wisdom about buying abroad was written for group one.

The contract mover’s reality

Let’s say your company is sending you to Abu Dhabi for three years. Or you’ve landed a 4-year contract in Doha. Or you’re heading to Singapore on a defined assignment with a renewal option that may or may not materialise.

Here’s the honest truth: for most contract movers, buying is almost never the right call, regardless of how attractive the market looks.

Why? Because property is illiquid, and transaction costs in most international markets run between 5% and 10% of the purchase price, sometimes more. That’s before legal fees, taxes, furnishing costs, and the time and stress of managing a sale from abroad when your contract ends. To simply break even on a purchase (not profit, just recover your costs) you typically need to hold for a minimum of five to seven years in most markets.

If your contract is two to four years, that window simply doesn’t exist. You’re not building equity. You’re absorbing costs.

There are exceptions, markets where appreciation has historically been fast enough to overcome transaction costs in a shorter window. But those same markets tend to be the most volatile. Betting on short-term price appreciation in an unfamiliar market, in a country where you’re not a permanent resident, is a high-risk strategy that rarely pays off the way people picture it.

The contract mover’s default strategy is straightforward: rent for the duration, rent well, and leave clean.

The financial energy you would have spent on a purchase is better used enjoying your time, building savings, and investing in markets you actually understand. That said, there is one scenario where buying makes sense even on a contract. We’ll get to that.

Why most people get this wrong

Whether you’re a lifestyle mover or a contract mover, the instinct to buy quickly is understandable. You’ve saved. You’re committed. Paying rent every month feels like throwing money away. And if you’ve done your research online, the neighbourhoods, the prices, the lifestyle, you feel ready.

But here’s what no amount of research can tell you before you’ve actually lived somewhere:

Which neighbourhood fits your daily rhythm, not the one that looks best in photos

Where your social life will organically form

What the commute feels like at 8am on a Tuesday

How the building sounds on a Friday night

Whether you love the country in January, not just the summer you visited

What the legal and financial landscape actually looks like on the ground

You don’t know what you don’t know. And in a foreign country, that gap is enormous.

The strategic case for renting first

Renting first isn’t hesitation. It’s due diligence.

Think of it this way: before a company makes a major acquisition, it runs months of due diligence. It doesn’t matter how good the deal looks on paper, you verify on the ground first. Your home abroad is one of the largest financial and emotional decisions of your life. Treat it with the same rigour.

Renting first gives you:

1. Real neighbourhood intelligence

You learn which streets feel safe at midnight, where the good local markets are, which areas are vibrant and which are dead by nine PM. This is knowledge you cannot buy from a distance. It only comes from living it.

2. Community before commitment

Your social life will shape where you want to live far more than any neighbourhood guide. Where you meet friends, find your gym, discover your coffee place: these anchor you somewhere specific. Buy before that happens and you risk being locked into the wrong location.

3. Financial clarity

Exchange rates shift. Tax treaties have nuances you only discover when you’re dealing with them. Local banking takes time to set up. Rushing into a purchase before your finances are properly structured in a new country is a genuine risk.

4. Legal and regulatory understanding

Property laws vary dramatically by country. Some nations restrict what foreigners can own. Some have inheritance rules that could seriously affect you. Some require a period of residency before you can buy. A few months on the ground lets you engage a good local lawyer without the pressure of an active deal on the table.

5. The option to change your mind

A significant percentage of first-time expats relocate to a different city or country within 18 months. That’s not failure, it’s the natural process of figuring out where you actually belong. If you rented, that pivot costs you almost nothing. If you bought, it could cost you everything.

How long should you rent? It depends on why you’re there

Here’s where the contract mover and lifestyle mover paths diverge clearly.

If you’re on a contract: rent for the full duration

For most people on a 2-4 year assignment, the answer is simple: rent for the entire contract period. Use months one to three to try different areas and get your bearings, then settle into something comfortable for the rest of your stay. The “throwing money away” argument sounds compelling, but the actual maths (transaction costs, legal fees, the risk of a forced sale at the wrong time) almost always makes renting the smarter financial choice for a defined-term stay.

The one exception: if your contract has a genuine likelihood of multi-year renewal and you are sincerely open to staying permanently, you can begin evaluating the market after 12-18 months, but only after running through the decision framework below. Even then, treat it as a lifestyle choice grounded in commitment, not a financial shortcut.

If you’re a lifestyle mover: minimum 6 months, ideal 12 months

The minimum is six months. Six months gets you through the honeymoon phase, those first two or three months where everything feels new and magical, and into the reality phase, where the cracks begin to show. You experience one season change, get a feel for the city’s social rhythm, and start building real connections rather than tourist-level ones. Leave before six months and you’re still a tourist making a tourist’s decision.

The ideal is twelve months. A full year is the gold standard because seasonality is real and chronically underestimated. A coastal town in southern Europe or Southeast Asia in July and that same town in January are practically two different places, different populations, different energy, different costs. A mountain destination in autumn can feel like a dream; in February it might feel isolating. You need to experience the full cycle before you commit capital.

Twelve months also gives you a full tax year to understand your obligations, enough time to build genuine friendships, and a clear sense of whether you’re staying permanently.

Extended, 18 to 24 months, for high-stakes or complex markets. In cities with intricate property regulations or high transaction costs, Dubai, Singapore, Hong Kong, the financial consequence of a wrong decision is too large to rush. This is equally true if you’re relocating with a family, where schools, healthcare access, and community networks take longer to properly evaluate.

It also depends where you’re moving to

The destination itself should heavily shape your strategy. Not all markets treat foreign buyers the same way, and not all carry the same risk profile. Here’s a clear-eyed look at the markets most relevant to international movers today, across the GCC and Asia.

The GCC

Dubai, UAE Dubai is the most open property market in the Gulf for foreign buyers. Freehold ownership is available in designated zones (and there are many of them) covering most of the areas expats actually want to live. The market is liquid by regional standards, there is no property tax, and mortgage financing is available to non-residents through UAE banks, though terms are less favourable than for residents.

That said, Dubai is still a contract-mover city at heart. The population is over 85% expatriate, turnover is high, and demand is closely tied to global business conditions. Transaction costs (agent fees, Dubai Land Department transfer fees, mortgage registration) typically run 6-8% of the purchase price on top of the property value. And the market has cycles: it has seen sharp corrections before and will again.

The honest read: if you are on a defined contract, rent. If you have been in Dubai for 12–18 months, have genuine long-term intent, have passed the five-test framework, and can hold for 7+ years, buying in the right freehold zone can make sense. But go in clear-eyed about the costs, the cycles, and what exit looks like.

Abu Dhabi, UAE Abu Dhabi’s property market for foreigners is more restricted than Dubai’s. Freehold ownership is limited to specific investment zones: Yas Island, Saadiyat Island, Al Reem Island, and a handful of others. Outside those zones, foreigners can access long-term leasehold (up to 99 years) in designated areas, but not outright ownership.

The rental market is well-developed and diverse. For most contract movers, renting across the full assignment period is the right call. For those with serious long-term intent and a focus on the designated zones, buying can work, but the restricted geography means your options are more limited than in Dubai, and the resale market is thinner.

Doha, Qatar Qatar has expanded foreign ownership rights in recent years, with freehold and long-term leasehold now available in designated areas including The Pearl, Lusail, and West Bay Lagoon. The developments are high quality and the market has grown meaningfully since 2020. However, Qatar remains a predominantly rental market for expats, the compound system is deeply embedded in how international families live, and for good reason: compounds offer community, security, schooling proximity, and flexibility in ways that ownership often can’t replicate at the same stage.

The key Doha-specific caution: the city is still maturing in terms of neighbourhood identity. Areas that feel right in year one may not feel right in year three as your life in Qatar takes shape. As Miguel’s story illustrates, locking in too early, even just on a lease, can cost you. Ownership amplifies that risk substantially. Rent first. Rent well. Get to know the city before you commit capital to it.

Riyadh and Saudi Arabia Saudi Arabia has historically been one of the most restricted markets for foreign property ownership in the Gulf. Non-residents cannot own property outside of designated tourism and investment zones, and the regulatory environment continues to evolve under Vision 2030. The expat housing market in Riyadh is heavily compound-based, with a strong, well-supplied rental market serving the international population.

For the vast majority of expats in Saudi Arabia, renting is not just the strategic choice, it is currently the only practical one. Monitor regulatory developments if you have long-term interest, but do not plan around ownership unless you have clear, current legal advice specific to your situation.

Bahrain Bahrain is one of the more accessible GCC markets for foreign buyers. Freehold ownership is permitted in a wider range of areas than most Gulf neighbours, and prices are considerably lower than Dubai or Doha. The market is smaller and less liquid, however, and Bahrain’s economic profile means demand is more sensitive to regional conditions. Worth exploring for long-term residents with genuine commitment, but thin resale liquidity is a real consideration.

Asia

Singapore Singapore has one of the most transparent and well-regulated property markets in Asia, but it is also one of the most expensive in the world, and foreign buyers face significant structural disadvantages. Additional Buyer’s Stamp Duty (ABSD) for foreigners currently sits at 60% of the property value on top of the purchase price. That is not a typo. It essentially makes speculative or short-term buying financially irrational for most expats. Long-term residents with permanent residency or citizenship face lower rates, but even then the market rewards patience and deep local knowledge.

The practical reality: most expats in Singapore rent, and the rental market is sophisticated and well-served. If you are on a corporate contract in Singapore, renting is almost certainly the right call for the full duration. If you are pursuing permanent residency and genuine long-term commitment, revisit the numbers at that point, with a lawyer who specialises in Singapore property and tax.

Hong Kong Hong Kong’s property market is among the most expensive per square metre on earth. Foreign buyers face no outright ownership restrictions, but Stamp Duty rates for non-permanent residents add a significant cost burden. Combined with extremely high entry prices and a relatively illiquid market at the high end, the holding period needed to break even on a purchase is long, typically well beyond a standard corporate assignment.

For contract movers, renting is the clear default. The rental market is developed, transparent, and offers access to the same neighbourhoods and quality of living that ownership would. For those with long-term permanent residency paths and genuine decade-plus horizons, the calculus changes, but that is a different conversation to have with a Hong Kong-based property lawyer.

Thailand Thailand is a market where foreign ownership rules genuinely catch people out. Foreigners cannot own land outright, the structures used to circumvent this (nominee shareholder arrangements, for instance) are legally grey and carry real risk. What foreigners can own freehold is condominium units, subject to the building maintaining at least 51% Thai ownership overall.

This means the entire landed property market (houses, villas, townhouses) is effectively off the table for straightforward foreign ownership. If you are relocating to Bangkok, Chiang Mai, Phuket, or anywhere else in Thailand, approach any purchase with serious legal advice and clear eyes about what you are actually buying, what your exit options are, and whether the structure you are using is robust.

Vietnam Vietnam allows foreign nationals to own property, but with important constraints. Ownership is capped at 50-year terms (renewable), foreigners are limited to no more than 30% of units in any one condominium building, and certain areas near military or security installations are restricted. The market in Ho Chi Minh City and Hanoi has developed rapidly, and there is genuine long-term potential, but the legal framework is still maturing, enforcement can be inconsistent, and title verification requires specialist local legal support.

For short to medium-term contract movers, renting is the clear choice. For those building a long-term life in Vietnam with serious intent, engaging a reputable local property lawyer from the start is essential, not optional.

Malaysia Malaysia is one of the more accessible markets for foreign buyers in Southeast Asia. The Malaysia My Second Home (MM2H) programme, while revised in recent years, remains a pathway for longer-term residents. Foreigners can purchase property, though a minimum purchase price threshold applies (which varies by state) and certain types of land remain restricted. Kuala Lumpur’s property market offers good value relative to Singapore or Hong Kong, the rental market is well-developed, and transaction costs are relatively moderate. Still, rent first. KL is a city where neighbourhood fit matters enormously, the traffic geography shapes daily life in ways that only become clear after living there, and the compound and condo community you choose has a large impact on your social experience.

Indonesia Indonesia applies some of the strictest foreign ownership restrictions in the region. Foreigners generally cannot own land freehold (Hak Milik title). What is available is Right to Use (Hak Pakai) for a limited period, or leasehold arrangements. Nominee structures are commonly used but legally risky. If you are relocating to Jakarta or Bali and considering a purchase, get specialist Indonesian property legal advice before going anywhere near a transaction. For the vast majority of expats in Indonesia, renting is not a strategic preference, it is the practical reality.

The core principle holds across every one of these markets:

Understand the destination’s legal framework, understand the costs of entry and exit, and understand the market from the inside before you commit capital to it.

The destination shapes the risk level and the rules. The principle doesn’t change.

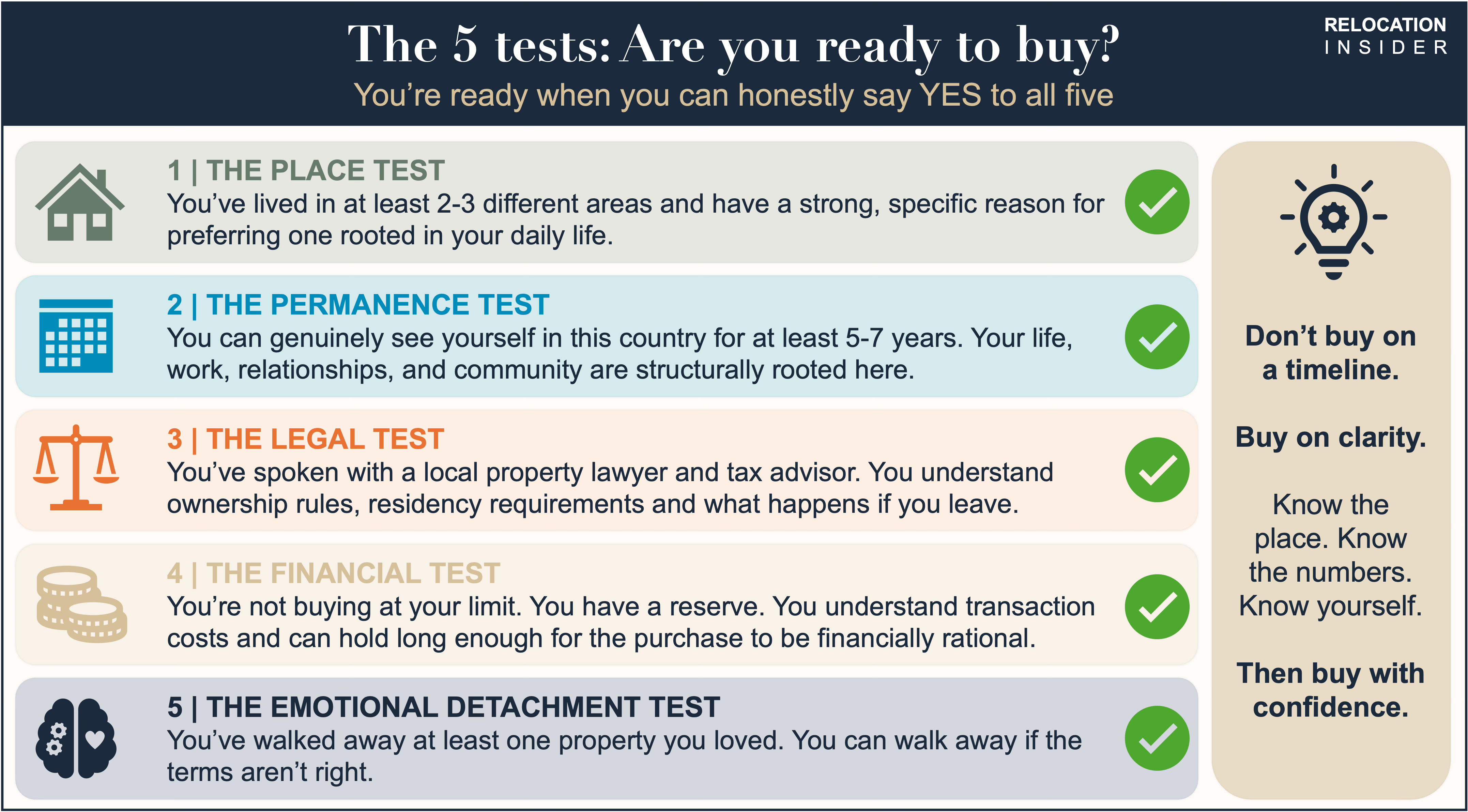

The decision framework: When are you ready to buy?

Don’t buy based on a timeline. Buy when you can honestly say yes to all five of the following tests.

The place test

You’ve lived in at least 2-3 different areas of the city or region and have a strong, specific reason for preferring one, not just “it feels nice,” but a reason rooted in your actual daily life.

The permanence test

You can genuinely see yourself in this country for at least 5-7 years. Not because you hope so, but because your life (work, relationships, community) is structurally rooted there. If you arrived on a contract, ask yourself honestly: is long-term extension genuinely likely, or are you telling yourself what you want to hear?

The legal test

You’ve spoken with a local property lawyer and a tax advisor, not just a real estate agent. You understand residency requirements, ownership structures, and what happens to the property if your contract ends and you leave.

The financial test

You’re not buying at the limit of your ability. You have a reserve. You’re not rushing because prices are rising, that urgency is a trap. And you’ve done the honest maths on transaction costs: can you hold long enough for the purchase to be financially rational?

The emotional-detachment test

You’ve walked away from at least one property you loved. If you can’t do that, you’re buying emotionally, not strategically. Emotional buyers get exploited. The ability to walk away is not weakness; it’s leverage.

The strategy (step by step)

Phase 1, Land and Explore (Months 1-3)

Rent furnished and short-term. Stay flexible. Go everywhere. This is pure orientation. Don’t sign anything long-term yet.

Phase 2, Settle and Test (Months 4-12)

Move into the neighbourhood that’s pulling you. Build real routines: the gym, the market, the coffee shop, the neighbours. Engage a lawyer. Start attending property viewings, not to buy, but to understand the market from the inside.

Phase 3, Evaluate (Months 10-12)

Run yourself through the five tests above. Be ruthlessly honest, especially the permanence test if you arrived on a contract. If all five are green, you’re ready to enter the market. If not, renew the lease and reassess in six months. No shame in that.

Phase 4: Buy with Conviction (When Ready)

By this point, you know the market, you know the neighbourhood, you have trusted local professionals around you, and you’re buying from a position of knowledge and strength, not urgency or FOMO.

The numbers don’t always say what you think

One final thing worth stating plainly: renting is not always the financially inferior option. The “throwing money away” narrative deserves a harder look than most people give it.

In many high-cost expat markets, the price-to-rent ratio makes purchasing mathematically irrational unless you’re staying ten or more years. In contract-heavy cities like Dubai or Doha, where employer housing allowances partially offset rental costs anyway, the financial case for buying is even weaker for most assignments.

In other markets, property appreciates quickly enough that early buyers genuinely win. But those markets tend to be the ones you can only properly evaluate after living in them, not before.

The point isn’t that renting is universally better. The point is that you cannot honestly evaluate the numbers until you understand the market from the inside. And that understanding takes time.

The bottom line for Relocation Insider readers

If you’re on a contract: rent for the duration. Use your energy to build a great life, not to manage a cross-border property transaction when your assignment ends.

If you’re a lifestyle mover: rent first. Give yourself at least 12 months. Use that time not as a waiting room but as a classroom, to learn the city, build your community, understand the legal landscape, and structure your finances properly.

In both cases: when you buy, buy because you know, not because you hope.

Miguel, for what it’s worth, figured it out. When the lease finally ended, he moved the family closer to the school, into a compound where the social fit was right and his wife had people around her. He didn’t make the same mistake twice. He took a short-term rental first, tested the area for three months, and only committed when he was certain.

He told me it transformed the whole experience. Not just logistically. Emotionally too. The family finally felt like they’d landed. The lesson he passes on to every friend who asks about moving abroad? Give yourself time to know the city before you let the city lock you in.

Great article, covers the topic clearly. I was a real estate broker for a portion of my life.